Understanding Murabaha: A Key Islamic Finance Structure

Murabaha is a popular Islamic finance structure that is sharia compliant and widely used in Australia and around the world. It offers a way to finance purchases without involving interest, which is prohibited in Islamic finance.

What is Murabaha?

Murabaha is a type of sale where the seller discloses the cost and profit margin to the buyer. This transparency ensures that the transaction is fair and sharia compliant. In a Murabaha agreement, the Islamic bank buys an asset and sells it to the customer at a higher price, which includes a profit margin agreed upon by both parties.

How Does Murabaha Work?

- Customer Request: The customer approaches the Islamic bank with a request to purchase a specific asset.

- Bank Purchase: The bank buys the asset from the supplier, taking ownership of it.

- Sale to Customer: The bank sells the asset to the customer at the original cost plus a pre-agreed profit margin.

- Deferred Payment: The customer pays the bank in instalments over an agreed period.

Benefits of Murabaha

Sharia Compliant

Murabaha is fully sharia compliant, as it avoids riba (interest) and ensures transparency in the transaction. This makes it an ethical choice for Muslims in Australia seeking Islamic finance solutions.

Fixed Profit Margin

The profit margin is fixed and agreed upon at the beginning of the contract, providing certainty and avoiding any hidden charges.

Wide Applications

Murabaha can be used for various purposes, including home financing, vehicle financing, and business investments. It is a versatile tool in Islamic finance.

Conclusion

Murabaha is a key structure in Islamic finance, offering a sharia compliant way to finance purchases. Its transparency and ethical nature make it a preferred choice for many Muslims in Australia. By understanding how Murabaha works, you can make informed decisions about your financial needs while adhering to Islamic principles.

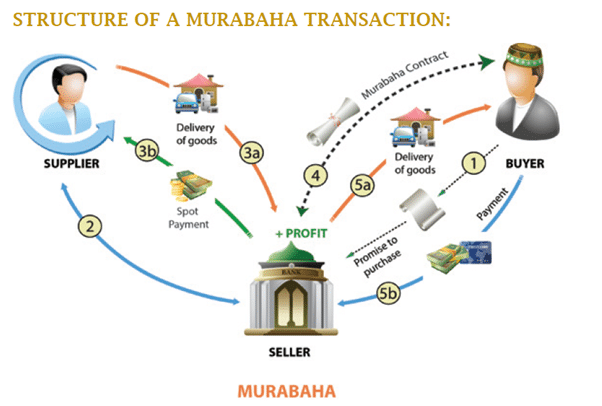

MECHANISM OF A MURABAHA FINANCE TRANSACTION:

- A customer needs certain goods and promises the Islamic bank to purchase the goods if the Islamic bank buys these goods from the supplier and takes the possession.

- The Islamic bank purchases the goods on the spot payment basis from the supplier and takes the possession (either constructive or physical).

- The Islamic bank sells the goods to the customer after adding its profit markup, on deferred payment basis for an agreed period.

- The customer makes the deferred payment to the Islamic bank after or during the agreed period.

APPLICATIONS OF MURABAHA CONTRACT IN ISLAMIC FINANCE:

Murabaha is one of the most widely used contracts at present in Islamic Banking and the investment sector. The various products where Murabaha is applied are as follows:

- Home financing

- Vehicle financing

- Project financing

- Goods financing

- Trade financing – LC based on Murabaha

- Profit rate swaps

- Islamic fund